Source: Shutterstock.

Source: Shutterstock.

Credit unions increased their share of consumer term loans in February, but their share of credit cards was unchanged, according to Fed data released Friday.

The Fed's G-19 Consumer Credit Report showed credit unions held $566.7 billion in non-revolving consumer loans Feb. 28, most of it in auto loans. In January, the Fed reported $565 billion in non-revolving consumer loans, and CUNA estimated $500.7 billion of that was in car loans, which credit unions have been originating at a much faster rate than banks in the past year. The rest are mostly unsecured personal loans.

Recommended For You

Credit unions' non-revolving consumer loans grew 19.1% from a year earlier — more than four times faster than growth at banks. The credit union balance grew 1.3% from January.

Banks held $930.5 billion in non-revolving consumer loans in February, up 4.4% from a year earlier and up 0.5% from January.

Credit unions' share of non-revolving loans was 15.7% in February, unchanged from January, but up from 13.9% a year earlier.

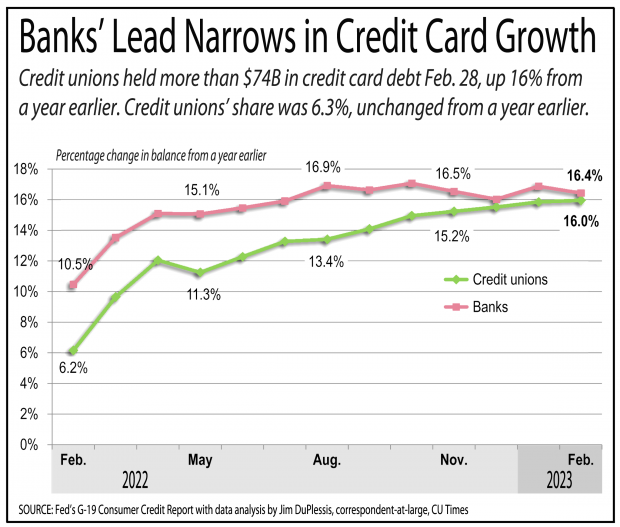

Credit unions fared worse with revolving consumer credit — credit cards.

Credit unions held $74.3 billion in credit card balances Feb. 28, up 16% from a year earlier and down 0.4% from January. The average January-to-February drop was 1.2% from 2015 through 2019.

Banks held $1.1 trillion in credit card debt, up 16.4% from a year earlier. The January-to-February drop was 1.1%, compared with an average drop of 2% for the five pre-pandemic years.

Credit unions had 6.3% of the credit card market in February, unchanged from a year ago or January. Banks had a 91% share in February, unchanged from January, but up from 90.5% a year earlier.

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.

Jim DuPlessis

Jim covers economic data trends emerging for credit unions, as well as branch news and dividends.