Source: Shutterstock

Source: Shutterstock

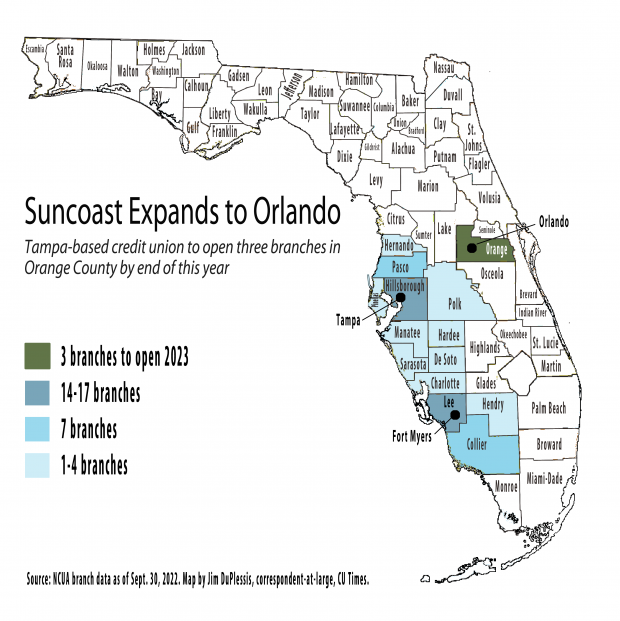

Suncoast Credit Union plans to expand into the Orlando, Fla., market this year, as other credit unions make similar moves elsewhere in the nation.

Suncoast of Tampa, Fla. ($16.2 billion in assets, 1.1 million members as of Dec. 31) announced Wednesday the locations of three new branches that it plans to open later this year.

Recommended For You

"Our ultimate goal is to reach and positively affect more members, and this expansion allows just that," President/CEO Kevin Johnson said. "We are passionate about the opportunity to bring the excellent financial services value of market leading rates and fee-free services to the Orlando market, and we know that this growth will allow our team to have greater impact on the financial lives of the individuals and businesses in these communities."

The new locations will have some employees who speak both English and Spanish. The service centers will also feature modern open floor plans, interactive teller machines and private office spaces for more personalized service that requires privacy.

Suncoast's 75 branches now stretch from just north of Tampa to just south of Fort Myers along the Gulf Coast. Nearly half of its branches are in Tampa and elsewhere in Hillsborough County and in Fort Myers and elsewhere in Lee County.

Truliant Federal Credit Union in Winston-Salem, N.C. ($4.1 billion in assets, 301,908 members) announced Jan. 27 that it betting heavier on an expansion in Upstate South Carolina than it announced last October.

Last fall, the credit union was going from one branch in Greenville County open since 1994 for workers at JPS Textile Group to five locations:

- The initial branch, which was moving to a new location in Greenville.

- An operations center in downtown Greenville that opened last fall.

- A branch at the Cherrydale Point shopping center, north of downtown, which opened in December.

- A branch in Easley, a Pickens County bedroom community, to open this spring.

- A branch in Greer, a bedroom community on Greenville County's eastern edge, to open in the fourth quarter.

Truliant said Jan. 27 it plans to add four more branches within three years. It didn't say where yet, except that they will be in the I-85 corridor, which runs through Oconee, Anderson, Greenville, Spartanburg and Cherokee counties.

That would bring its total locations in South Carolina to nine, and it said it wants to have 10 or more in the Upstate eventually.

"The Upstate's remarkable economic development and continued population boom make it ideal for this expansion. These new locations will provide us with an even stronger foothold in the state," Truliant President/CEO Todd Hall said. "By swiftly matching the region's fast-paced growth, we intend to reach even more potential members and give them the financial tools they need to build a brighter financial future."

The Upstate represents the fourth regional concentration of Truliant branches along with southwestern Virginia, the Charlotte-Metro area, and its home in North Carolina's Piedmont Triad of Winston-Salem, Greensboro and Highpoint.

Nationally, credit union assets grew 5.2% to $2.2 trillion as of Dec. 31, while membership rose 4.5% to 138 million. Growth was much faster at most of the credit unions announcing branch expansions.

Suncoast's assets grew 9% to $16.2 billion as of Dec. 31, and members grew 10.1% to 1.1 million. Truliant's assets grew 9.3% to $4.1 billion, and members grew 5.5% to 301,908.

Other credit unions announcing expansions included:

Blue Federal Credit Union of Cheyenne, Wyo., which opened its 20th branch Jan. 21 in Superior, Colo., 20 miles northwest of Denver. The credit union now has 12 branches in Colorado and eight in Wyoming (in addition to its headquarters). Its assets grew 13.6% to $1.8 billion, as members grew 7.1% to 117,577.

Utah Community Federal Credit Union of Provo, Utah ($2.8 billion in assets, 231,894 members), which plans to open a new branch in Vineyard, eight miles north of Provo, this spring. The credit union's assets grew 12.1% to $2.8 billion, and members grew 4.7% to 231,894.

Brooklyn Cooperative Federal Credit Union of New York, which opened a branch Jan. 17 at Chestnut Commons, an affordable housing development managed by Cypress Hills LDC. This is the third branch for the credit union, which serves low-income neighborhoods with the goal of providing fair and affordable financial products that directly address market gaps, building assets and resilience in their local communities. Its assets last year fell 7.1% to $51.4 million, and members fell 3.7% to 7,574.

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.

Jim DuPlessis

Jim covers economic data trends emerging for credit unions, as well as branch news and dividends.