Independent Community Bankers of America's website. (Source: Adobe Stock)

Independent Community Bankers of America's website. (Source: Adobe Stock)

Just five days after the $1.5 billion Scott Credit Union in Edwardsville, Ill., signed a definitive purchase and assumption agreement to acquire the $92.9 million Tempo Bank in Trenton, Ill. on Aug. 20, the Independent Community Bankers of America used the $14 million transaction to launch another call for lawmakers to address the growing trend of credit union-bank acquisitions.

In the ICBA's Aug. 25 press release, the headline read: "As Credit Union-Bank Acquisitions Top 100, ICBA Urges Washington to Act."

Recommended For You

But it appeared the ICBA's definition of a credit union-bank acquisition is somewhat expansive. It turned out that the ICBA's list of credit union-bank purchases include not only "whole bank" acquisitions, but credit unions that only bought branches and/or certain assets and liabilities of the bank.

However, the list, which CU Times requested and received from the Washington, D.C.-based community banking group, also included credit union-bank deals that were called off and at least one deal that was counted twice.

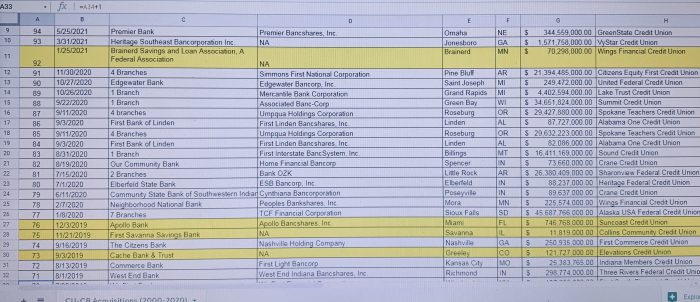

The ICBA listed 101 deals, which started on Sept. 16, 2003, when Spokane Teachers Credit Union in Liberty Lake, Wash., bought one branch from Community Financial Group based in Cabot, Ark. The list ended with the proposed acquisition deal of Tempo Bank by Scott CU on Aug. 20, 2021.

But a review of the ICBA list found there were only 41 finalized credit union purchases of "whole banks," or the majority of the bank's assets and liabilities, acquired from 2011 to the end of 2020. CU Times did not include the proposed 11 credit union bank buy deals announced this year because they have not been finalized.

The ICBA list included an acquisition in 2011 when United Federal Credit Union in St. Joesph, Mich., announced it was buying Griffith Savings Bank, which launched the slow but growing trend of credit union bank acquisitions. That first deal was completed in 2012. The ICBA listed this transaction as an acquisition of an asset or branch, not as a whole bank buy.

As of June 30 of this year, a spokesperson for the NCUA said the independent federal agency has approved 41 whole bank acquisitions by credit unions since 2012.

Interestingly enough, the ICBA listed 28 credit union-bank buy deals as "acquisition of whole company" (incl. Majority Stake) transactions from 2012 to 2020. However, the FDIC reported that since 2015, it has approved 32 whole bank acquisitions by credit unions.

"The ICBA list includes some mergers as whole bank when the majority of the assets/liabilities were acquired," an FDIC spokesperson said. "In our system of record, many of these will be treated as partial mergers."

The FDIC said its records show that it has approved 24 partial acquisitions of banks by a credit union, and from 2003 to 2014 there were an additional 11 partial acquisitions approved by the FDIC.

The ICBA list included 36 deals in which credit unions bought branches from 2003 to 2020. In more than half of those deals, 21 credit unions bought only one or two bank branches. Seven credit unions purchased three to five bank branches, and eight credit unions acquired seven to 11 bank branches.

The ICBA also listed six deals in which a credit union bought "certain assets and liabilities."

What's more, the ICBA also included on its list at least seven credit union-bank acquisition agreements that have been called off.

ICBA's CU/Bank Purchase spreadsheet includes called-off bank purchases in its official count.

ICBA's CU/Bank Purchase spreadsheet includes called-off bank purchases in its official count. In 2020, for example, the acquisition of the Neighborhood National Bank in Mora, Minn., by Wings Financial Credit Union was cancelled by the Apple Valley, Minn.-based credit union without any explanation.

And while 2019 was the industry's high mark of 16 announced credit union-bank acquisition agreements, that number was cut down to 13 credit union-bank purchase deals because at least three of them had been cancelled, including Apollo Bank in Miami by Suncoast Credit Union in Tampa, Fla.; First Savanna Savings Bank in Illinois by Collins Community Credit Union in Cedar Rapids, Iowa and Cache Bank and Trust in Greely, Colo., by Elevations Credit Union in Boulder.

Three additional deals that had been called off included Southern Bank in Sardis, Ga., by SRP Federal Credit Union in North Augusta, S.C., Citizens State Bank of Ontonagon in Michigan by Honor Credit Union in Berrien Springs, Mich., and State Bank in Green River, Wyo., by Trona Valley Community Federal Credit Union, also based in Green River. These deals were announced in 2017.

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.

Peter Strozniak

Credit Union Times reporter covering credit union operations, fraud, M&As, leagues, business continuity, and breaking news.