Source: Shutterstock.

Source: Shutterstock.

Credit union business lending isn't concentrated among the nation's largest; it's actually weighted to the center.

One example is GECU Credit Union of El Paso, Texas ($3.4 billion in assets, 399,106 members). GECU's commercial loans on June 30 stood at $58.3 million, up 45% from a year earlier and accounting for 2% of total loans. Its total loans on June 30 were $2.6 billion, up 3%.

Recommended For You

It's not an outlier.

Greater Nevada Credit Union of Carson City ($1.3 billion in assets, 77,511 members) launched Greater Commercial Lending in 2017 to help member credit unions offer commercial loans, including federally guaranteed loans through the USDA and Small Business Administration. The Reno, Nev.-based CUSO has a network of lenders that includes 10 credit unions with $9 billion in assets and 645,201 members from Kalamazoo, Mich., to Baton Rouge, La.

In September, Member Business Financial Services, a Philadelphia-area CUSO, launched Nu Direction Lending, LLC, with the help of a fintech that will enable it to offer business owners the ability to apply online or with their mobile devices for loans usually considered too small or too complex for credit unions to handle. It's designed to provide small loans to feed the growth of successful companies without relying on real estate collateral, which accounts for the vast bulk of credit union business loans.

The CUSO is owned by 13 credit unions ranging from American Heritage Federal Credit Union ($3.1 billion in assets, 209,737 members) based in Philadelphia to American Spirit Federal Credit Union ($77.8 million in assets, 13,225 members) based in Newark, Del., home of the University of Delaware's Fighting Blue Hens and 60 miles southwest of Center City Philadelphia.

When credit unions are ranked by assets and sorted into three groups of roughly equal size, GECU, Greater Nevada and American Heritage fall into the bucket of medium-sized credit unions of $1 billion to less than $4 billion in assets. That group contained 31% of the movement's 124 million members and 32% of its $1.77 trillion in assets as of June 30, based on an analysis of NCUA data by CU Times.

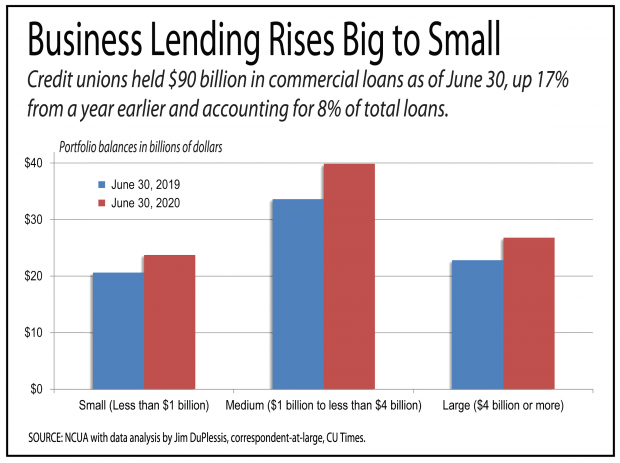

Mid-sized credit unions held at $39.9 billion in commercial loans at June 30, a gain of 18.5% from a year earlier, and those loans accounted for 10% of their total loans. Their total loans at June 30 were $386 billion, up 8%.

In both smaller credit unions and larger ones, commercial loans had a much smaller place among their portfolios, and their growth rates for commercial loans were slightly lower.

Small credit unions (less than $1 billion in assets) held $23.8 billion in commercial loans as of June 30, up 15.2% from a year earlier and accounting for 7% of total loans. Their total loans as of June 30 were $324.3 billion, up 4.3%.

Large credit unions ($4 billion or more in assets) held $26.8 billion in commercial loans as of June 30, up 17.6% from a year earlier, and accounting for 6% of total loans. Their total loans as of June 30 were $438.6 billion, up 8.4%.

GECU got into business lending about 20 years ago, and did well for about five years as the economy boomed. "We didn't know what we were doing, but we didn't know it," Chris Tompkins, GECU's SVP and chief commercial services officer, said.

That realization was delivered by the Great Recession that started in December 2007. "Once the financial meltdown occurred, a lot of weaknesses were exposed," said Tompkins, who participated in a webinar Thursday on recent research on commercial lending from the Filene Research Institute in Madison, Wis.

The research published by Filene showed that about 500 credit unions offered "basic business services" defined as including business checking and savings accounts, business lending, business credit cards and basic online banking.

They found several that offered "semi-comprehensive business services" that include ACH payment processing, remote deposit capture, automated payroll and tax management, investment services and "robust online banking."

None had the "comprehensive business services" of big banks, which include fraud and data management, automated account reconciliation, returned item management, zero-balance accounts, advanced online security and accounting features.

After the Great Recession ended in 2009, many banks had left the El Paso market. GECU stayed and continued to build its connections to members who owned small businesses. Now it has started moving from providing basic services for businesses to a "semi-comprehensive" level of services, including remote deposit capture and ACH capabilities.

Without those services, Tompkins said GECU has no chance of drawing members with larger businesses, and more of the El Paso market's $1 billion in business checking accounts

"They would pick us, but we just don't have what they need," he said. "There's a large market we could serve if we just have the products and services. We offer products that are primarily for very small, mom-and-pop businesses."

GECU provided many Paycheck Protection Program loans to businesses. Of course, the operation wasn't designed to generate income, but it did serve to get out the word that GECU was available to help area businesses.

Lack of visibility is a widespread barrier for credit unions seeking to serve businesses. "Sometimes we're not thought of at all, or we're the lender of last resort when the others have turned them down."

Many other barriers to credit unions doing more business lending are cultural, Tompkins said. For one thing, "credit unions tend to be risk-averse," which he said is a byproduct of the inexperience of credit union management.

"Nobody has an appetite for a risk to do something they don't understand," he said.

Another barrier is the cost of acquiring expertise to be credible and competent. A business finance manager is usually still in the beginner stage in their first three to five years of their career.

But hiring talent, experienced or fresh out of college, will require that credit unions be willing to pay the market rate – or more in some cases.

A young person wanting to be a commercial lender tends to envision working for a bank, and might consider a credit union to be a drag on their career.

"Commercial lenders are the highest-paid people in a bank, so they're going to be the highest-paid people in a credit union," he said.

Tompkins said commercial lending "isn't rocket science," but it is both more complicated and nuanced, requiring judgment that only experience can provide.

While a mortgage or car loan might have five different ways to evaluate ability to repay, there are perhaps 100 methods for businesses. However, only about 12 are relevant, and the trick is to figure out which of the 100 fit the case.

Another barrier might be banks and their lobbyists. Tompkins said banks have "allowed" credit unions to do what they didn't want to do, like making auto loans, "as long as they didn't do what they wanted to do."

Now, as credit unions have "jumped into their sandbox" of commercial lending, expect bankers to be unhappy, he said.

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

Jim DuPlessis

Jim covers economic data trends emerging for credit unions, as well as branch news and dividends.