Source: Shutterstock.

Source: Shutterstock.

While the pandemic led to an unprecedented recession, its uneven impacts were experienced acutely in the automotive industry.

The whacky conditions have led to rising used car prices, and sharp drops in lending market share for banks and credit unions. Preliminary numbers for July from Experian showed both banks and credit unions regaining some share, but still below pre-pandemic levels.

Recommended For You

U.S. factories shut down less than a week after COVID-19 was declared a pandemic on March 11, and slowly began reopening in June. As supplies of new cars fell, buyers were pushed into the used car market.

The growing crowd of used car buyers drove up prices. The axiom of fast, steady depreciation of used cars was run off the road as used car values rose.

But buying a car was difficult. First, many dealers had to either close down their showrooms completely or limit access as a health precaution.

If you were lucky to keep your job and maintained a good credit score, the market was your oyster. If you needed a car to have any hope of working but had a spotty credit score, you were chum in a shark tank.

Banks and credit unions tightened lending standards, while automakers increased incentives for prime borrowers.

As banks and credit unions got pickier about borrowers, those with lower credit scores went to finance companies or buy-here-pay-here car lots for used cars, said Melinda Zabritski, an automotive analyst for Experian, an Irish company that provides credit reporting and marketing services.

Prime borrowers (FICO scores of 661 to 779) paid an average interest rate of 6.05% in the second quarter on used cars, down 49 basis points from a year earlier. Subprime borrowers (500 to 600) paid 17.78%, up 42 bps, according to Experian.

Therefore, bank and credit union market shares dropped sharply in the spring:

- Credit unions held 12.1% of new car loans and leases in February, but their share fell to a low of 9.8% in June, with July showing an improvement to 10.6%.

- Banks followed the same pattern, falling from 30.4% of new car financing in February to 22.8% in June and rising to 24.5% in July.

- Captives had the opposite pattern: Rising from 52.2% in February to 63.5% in June, and falling to 60.8% in July.

- Credit unions experienced similar trends in used car financing, where they are strongest. They held 24.9% of deals in the second quarter, down from 26.1% a year earlier and 28.4% in 2019′s fourth quarter.

- Banks did not show an impact from the pandemic in used cars. They had 34.8% of loans in the second quarter, unchanged from December but down from 36.4% in 2019's second quarter.

Much of the share was given up by strategy, Zabritski said. This includes lenders verifying employment more carefully and tightening loan-to-value limits.

"For many of the lenders I've talked with, there's been a purposeful move away from subprime," she said.

Unlike the Great Recession, which was precipitated by a financial crisis, this one was entered as banks and credit unions were enjoying record earnings.

"We're in unprecedented times," she said. "We've never had a situation where dealers had to close, where consumers couldn't go out and transact. But we're also in a situation where lenders have funds."

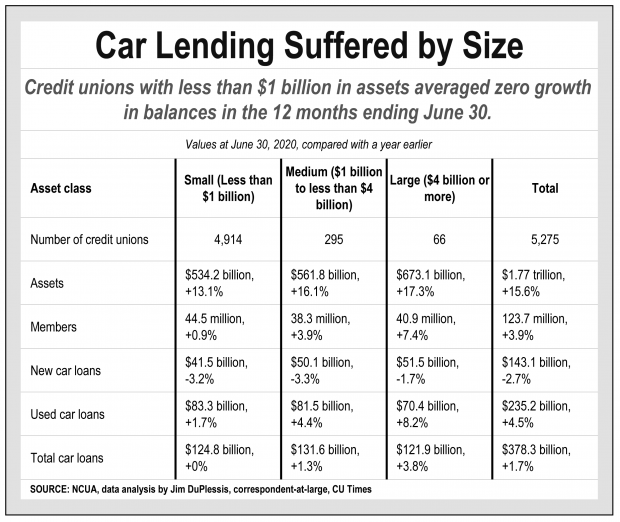

Among credit unions, car loan balance trends improved by size, according to an analysis of NCUA data by CU Times.

Among those with less than $1 billion in assets — a mark chosen to capture about a third of the movement's assets and members — total car loan balances were flat from 2019's second quarter to 2020's second quarter. They grew 1.3% for medium-sized credit unions ($1 billion to less than $4 billion in assets), and 3.8% for the largest credit unions.

New car loan balances decreased for each class, with the drops diminishing by size, and used car loans grew for each, with the gains improving by size.

Another curious artifact of this command recession is that many borrowers have maintained good credit scores even without jobs, thanks to the boost from the $600-a-week federal unemployment benefits and lender forbearances. But the impasse between the Democratic-controlled House and Republican-controlled Senate resulted in those benefits expiring in at the end of July. And forbearances will run their course, too.

Zabritski said delinquency numbers mean little now, making it difficult to predict charge-offs. But she expects lenders to start repossessing more cars by the end of the year as pandemic-related accommodations expire.

Other numbers are starting to show the automotive market returning to something resembling pre-pandemic levels.

More 2021 model year vehicles are making their way into dealerships as automakers ramp up production, and new car prices have started to drop. Used car prices are still rising, but they should start falling in the coming weeks, according to Edmunds, a car-buying analytics company based in Santa Monica, Calif.

The average list price for 2017 model year vehicles climbed to $24,287 in August, up $721 from July and nearly $1,500 from June.

"Come October and November, some of the lease extensions that consumers opted into at the start of the pandemic will expire, so more off-lease vehicles will be hitting the market," Ivan Drury, Edmunds' senior manager of insights, said.

"Bigger discounts on 2020 model year vehicles should create downward pressure on the used market, and depreciation for used vehicles typically accelerates during the fourth quarter, so used prices and values are likely going to drop."

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.

Jim DuPlessis

Jim covers economic data trends emerging for credit unions, as well as branch news and dividends.