Community banks get the best deals.

Community banks get the best deals.

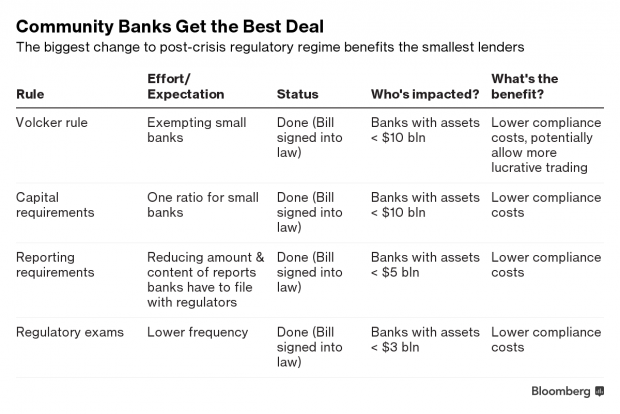

President Donald Trump just took another step in his 15-month push to ease regulation of banks, this time putting his signature on the most far-reaching measure yet to loosen rules prompted by the global financial crisis.

Trump signed into law on Thursday a bill that provides community and regional banks with relief, exempting them from significant oversight. Last year, he pledged to "do a big number" on the 2010 Dodd-Frank Act, the bedrock law enacted to prevent a future financial meltdown. Yet the latest move is relatively restrained, leaving most of the act intact.

Recommended For You

And much is still afoot beyond Dodd-Frank: Some U.S. rules have been delayed and others enforced with less vigor, while regulators slowly move to implement more deregulatory recommendations made in a series of Treasury reports. Here's a summary of what's happened so far, or may happen in the weeks, months and years ahead.

A core element raises the threshold established in Dodd-Frank for being considered a systemically important bank — a label that imposes annual stress testing and other requirements on firms. Lifting the threshold to $250 billion from $50 billion will also likely benefit mid-sized regional banks, which will face fewer restrictions and lower compliance costs.

"Large regional banks are getting meaningful easing from regulations in this bill as well as from the stress tests," said Chris Wolfe, a managing director at Fitch Ratings. "They're probably the biggest winners."

There are a few elements in the new legislation that Trump signed into law this week that also helps the largest banks, though most of their attempts to get further concessions from legislators failed. There's "not a whole lot" for the biggest firms in the bill, according to Citigroup Inc.'s Julie Bell Lindsay.

"Deregulation isn't the right word," said Lindsay, who's deputy head of regulatory affairs. "All components of post-crisis regulation will remain in place. This is just re-calibration and re-balancing to eliminate some unintended consequences we've observed."

Among the top goals of Dodd-Frank was ending bailouts of "too-big-to-fail" firms whose collapse would risk bringing down the rest of the financial system. In addition to Dodd-Frank, global regulators revised the international capital regime known as Basel and introduced liquidity rules for all of the largest banks worldwide to follow.

U.S. regulators went further in implementing those global standards, gold-plating some of the elements such as the minimum level of debt that can be written off to help re-capitalize a failing bank. The Treasury has recommended dialing back a lot of those rules, and regulators have addressed some, though progress has been slow.

Another element of post-crisis reforms was to protect consumers and small investors from abuse after predatory lending contributed to the housing bubble and its collapse. Some of the enforcement has already been curtailed, but rule changes have been restricted to a few that were enacted toward the end of the previous administration's tenure, using a maneuver which lets Congress overturn regulation soon after it's adopted.

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.