Based on results from first quarter 2014, the current forecast for financial institutions everywhere indicates a regulatory warming trend with a chance of increasing enforcement activity in the months ahead.

Such was the prediction during a recent Quarterly Regulatory Compliance Briefing webinar sponsored by Continuity Control, a compliance management system for credit unions and banks. A quiet fourth quarter 2013 has given way to a distinct uptick in activity with a chance of increased fallout for financial institution boards of directors less diligent in their duties.

"It's been a very interesting and somewhat unusual quarter," said Pam Perdue, Continuity Controls' EVP of regulatory insight and co-presenter at the April 10 webinar. "Yes, things are steadying a bit, but there is a lot of ground to make in the coming months."

Recommended For You

Utilizing data from the Banking Compliance Index the company uses to measure regulatory impact, Perdue noted a rise in key indicators driving the index. While the changes may not return credit unions and banks to the hectic compliance climate that characterized the first part of 2013, first-quarter 2014 increases show that a regulatory activity is once again gaining steam.

"The enforcement climate was warm during the end of last year, but now it's time to turn the dial back up to 'hot,'" Perdue said.

The official Q1 2014 BCI score was 1.69 – the number of FTEs required by the average financial institution to manage compliance obligations. The BCI score is up from 1.61 during an unusually quiet fourth quarter, but doesn't come close to matching the score of 2.35 during the same period in 2013, a high due largely to mortgage reform activity, Perdue said.

However, any further chance of decline from the current number is unlikely, she said.

"This is the new norm," she said, "For those of you thinking that you can close your eyes, click your heels and head back to Kansas; Dorothy, that's probably not going to happen."

The 5% increase in the FTE "consumption" score, as it is called, is accompanied by a rise in the per-institution incremental compliance cost during first quarter to $37,621, up from $35,798 during the preceding quarter.

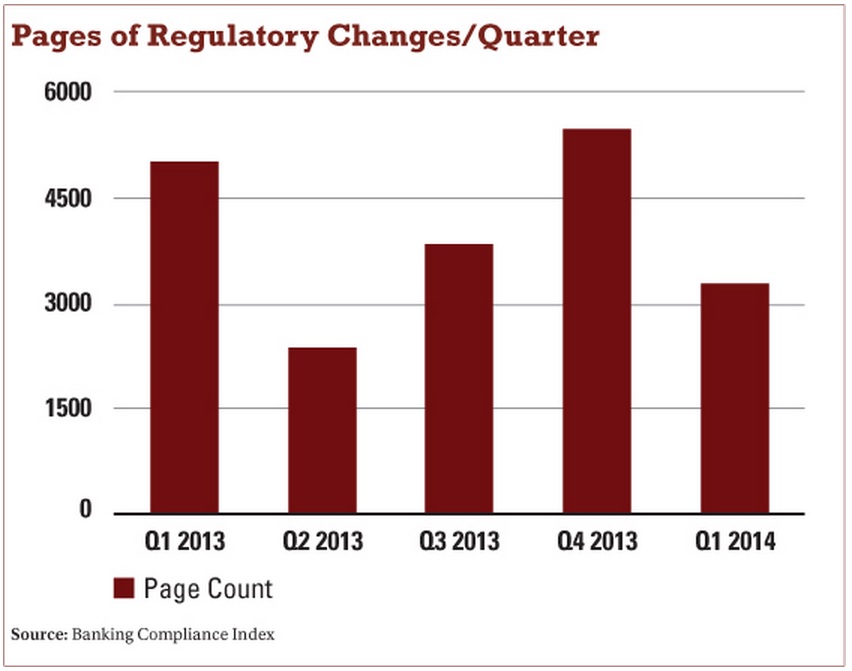

But the number of enforcement actions climbed 9.69% to 165, up from 134 previously. The average number of items rose to eight per enforcement action, up from seven in the previous quarter.The first quarter also saw the addition of 3,284 additional pages of regulatory requirements, down from 5,507 pages added during the fourth quarter.

"When it comes to enforcement actions, all things old are new again," Perdue said. "Issues involving the Bank Secrecy Act and safety and soundness dominated examiners' agendas."

Both measures are shown in the charts at left. (Click on the charts to expand.)

Another company's measure similarly found activities heating during the first quarter.

That would be Exam Watch, a financial peer-to-peer information sharing program on the cbanc Network, a free and secure online source of problem-solving content authored by banking and credit union professionals. Of the 142 banks and nine credit unions reporting during first quarter, 28% raised concerns about increased regulator scrutiny of their boards of directors, according to Matt Schriner, cbanc Network's managing editor and a webinar co-presenter.

Board training and the thoroughness of board meeting minutes were top areas of concern. Board involvement in key credit union issues, including compliance matters, also drew examiners' attention, Schriner said. He encouraged webinar participants not to underestimate regulator concerns in these areas.

"Make sure all employees and board members receive annual training," said Schriner, paraphrasing one Exam Watch entry. "Examiners want to see that training reflected in appropriate detail in board meeting minutes."

Compliance discussions at board meetings also are gaining importance for examiners, Schriner said. Those discussions also need to be reflected in the meeting's minutes in appropriate detail.

"Make sure that committee meeting minutes are equally detailed and flow up to the board meeting minutes," he added.

Most regulatory action issues during first quarter were relatively minor compared to those from previous year. The one exception, not surprisingly, was guidance on Bank Secrecy Act expectations regarding marijuana-related businesses issued by the Financial Crimes Enforcement Network.

A Justice Department memo outlined requirements for the 20 states and District of Columbia that have some form of legal marijuana usage. "This is a pretty heavy-lifting area," said Schriner.

Compliance with Basel III Tier 2 Capital and Subordinated Debt requirements also generated discussion during the webinar. Perdue also briefly discussed the NCUA's guidance for federal credit unions that want to use derivatives to manage interest rate risk, reminding institutions of their purpose in the agency's eyes.

"Derivatives are available to credit unions only for this limited use and should not be considered for any other form of activity," she said.

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.