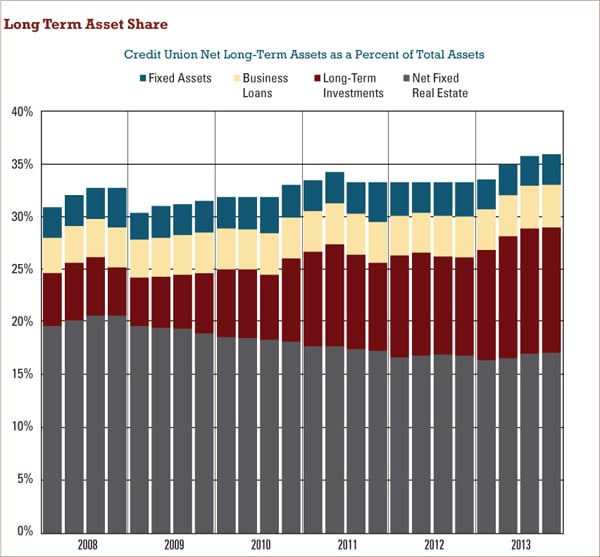

While mortgage loans still make up the majority of credit unions' long-term asset portfolios, fixed assets, business loans and other long-term investments have grown beyond 35% of the industry's overall balance sheet.

While mortgage loans still make up the majority of credit unions' long-term asset portfolios, fixed assets, business loans and other long-term investments have grown beyond 35% of the industry's overall balance sheet.

That level raises a red flag for regulators concerned about interest rate risk exposure.

Credit union executives and consultants have decried as arbitrary NCUA's 35% tipping point, but the prescription for potential balance sheet ills is not that simple and not without other considerations, said John Worth, the NCUA's chief economist.

Recommended For You

Mitigating credit union risk is a major part of regulatory oversight, and fixed-rate mortgage loans and other long term assets can pose a significant threat to credit unions that haven't balanced them with short-term deposit growth and other strategies, he said.

Despite credit union gains in real estate market share, residential mortgage loans have declined as a percentage of the industry's overall investments in long-term assets, Worth said. Since 2008, net fixed-rate real estate loans have dropped several percentage points as overall long-term asset portfolio numbers continued to climb. (Click on graph above to enlarge.)

Also of Interest:

Filene Exclusive: Credit Unions Navigate Choppy Lending Waters

NCUA's New Rules in 2013: Year in Review

Long Run Seen for 30-Year Mortgage: On-Site at MBA

Worth further explained the NCUA's application of the 35% tipping point.

"We don't supervise by single, potentially arbitrary numbers," Worth said. "It's all about balance sheet management and your strategy to deal with this configuration, but 35% net long-term assets puts a credit union above the 75th percentile of that distribution. At that point examiners should be asking questions."

Over the past two years, EVP/CFO Denise McGlone of the $2.3 billion Affinity Federal Credit Union has chosen to mitigate credit union risk in several ways, including selling off part of her long-term, fixed-rate mortgage loan portfolio. The sale was driven in part by the need to strike a better balance among assets and liabilities in the face of eventually rising interest rates.

It was also done as a concession to her regulator.

"NCUA pushed us a little bit, but I would say they just escalated our timing," McGlone said. "I wasn't comfortable with all that risk."

In 2011, Affinity's $1.8 billion loan portfolio included $1.3 billion in residential fixed-rate mortgages with 30-, 20- and 15-year terms. By 2013, the portfolio value had dropped to $1.7 billion with $1.1 billion in mortgage loans, a $200 million reduction due largely to the loans' natural amortization and sales of the longer duration loans, according to Richard Chin, Affinity's vice president and treasurer.

"The sales were part of our interest rate risk management strategy," Chin said. "The regulators just encouraged us to sell sooner than we wanted."

Read more: California CU gives up $3.3 million in annual interest income

Henry Wirz understands the value of a second opinion on his balance sheet. As CEO of the $1.9 billion SAFE Credit Union in North Highlands, Calif., Wirz employs an interest rate model that he said shocks the credit union balance sheet by 400 basis points in either direction of the current interest rate to measure the potential financial risk to the credit union at many levels.

SAFE has hired Dallas-based ALM First Financial Advisors to run the balance sheet analysis. Before and after the process, the credit union relies on Wilary Winn LLC, a risk management consulting firm based in St. Paul, Minn., to evaluate assumptions the credit union inputs into the risk module and then recheck the calculations and compare them to the ALM First results, Wirz said.

The veteran executive tends to be critical of NCUA's approach, wondering if the regulator brings similar thoroughness to the process.

"It seems to me that NCUA instead looks at balance sheet ratios and assumes that certain ratios are too high given the risk of higher interest rates," Wirz said. "That is a false premise. The only reasonable way to measure interest rate risk is to look at the entire balance sheet and model impact on net economic value and on net interest income holding the balance sheet steady and assuming an instant rate increase across the yield curve."

However, SAFE, too, sold off real estate mortgage loans to the secondary market as a way to mitigate balance sheet risk. The sales had no small impact on the credit union's bottom line.

As of year-end 2013, SAFE had a total loan portfolio worth slightly more than $2 billion, of which first mortgage loans comprised a little more than $502 million. In addition, the credit union holds about $72.4 million in home equity loans, for a total of about 45% of the total portfolio.

By this past December, SAFE had sold off $269 million in real estate loans as part of its balance sheet risk mitigation strategy. Although it still earns $3.8 million annually for servicing those loans, Wirz estimates that the sale cost the credit union about $3.3 million in annual interest income.

"We took substantial penalty in order to avoid interest rate risk," Wirz said. "Depending on how fast the cost of funds increases, we may be forgoing substantial future income."

Wirz believes that NCUA's 35% measure, in practice if not in theory, is still an arbitrary metric that some field examiners use to enforce their supervisory guidance. Moreover, its enforcement can be a detriment to member service.

"NCUA wants to keep us safe and sound. Hurray for that!" Wirz said. "I believe we need to manage risk, but I think the way NCUA is doing it is patently wrong."

A flat-out arbitrary percentage, whether intended or not, will find credit unions on the wrong side of both the member-service and income equation almost every time, he said.

"You will disappoint members and not be competitive in the marketplace, and you're going to forego income to which you otherwise were entitled," Wirz added. "Our job is not to gamble with interest rates, but to manage them," he added. "There is a qualitative difference between the two."

Read more: Other IRR management options …

In many cases, selling off mortgage loans is not a financially wise or even logical solution, especially for larger credit unions that have other risk-hedging options available to them, according to Peter Duffy, a managing director with Sandler O'Neill and Partners, a New York City-based financial consulting firm. Other hedging tools available, including NCUA's new ruling on using derivatives, provide more effective and less costly alternatives, especially in preparing for the uncertainty caused by rising rates, he said.

"When rates go up, there is a decent likelihood that it will be a highly stressed balanced sheet environment like we've never seen before," Duffy said. "Prudent managers will have already anticipated what it will be like and have prepared their balance sheets in every manner possible."

Credit unions also can increase the amount of securities available for sale, and increase reliance on amortizing investments while reducing reliance on callable agency securities. They also should consider the role of longer-term advances from the Federal Home Loan Bank depending on the institution's overall liquidity and the ability to meet projected withdrawals in a rising-rate environment.

In that consideration, institutions should include in their analysis any investment portfolio restructure that better prepares their balance sheets for the change. Using derivatives to hedge balance sheet risk is also an option given the new rule, Duffy said.

"In our environment, earnings are increasingly more difficult to come by, so we have to run our balance sheets to realize the optimum balance for all these priorities," he said. "That's why analysis needs to be rigorous and why it's beneficial to have more than one opinion."

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.