Driving through the streets of Southern California, an interesting dining phenomenon reveals itself. Many restaurants advertise an unexpected combination of food choices, often at cheap prices. Ice cream for a dollar, Chinese food, burgers, and donuts, the signs read. If you've ever stopped into one of these places you quickly realize that their variety is rarely matched by their quality. They try to be too many things to too many people.

Many credit unions fall into this same trap, albeit not because of glazed donuts or egg rolls. The "all things to all people" philosophy emerges when credit unions attempt to invest heavily across all conceivable delivery channels without really serving members effectively through any of them.

Recommended For You

In the report, Channel Delivery for Tomorrow, Ben Rogers, research director at the Filene Research Institute, explores how credit unions should adapt to changing consumer preferences around delivery channels while improving organizational excellence and efficiency.

Click on the graph below to expand.

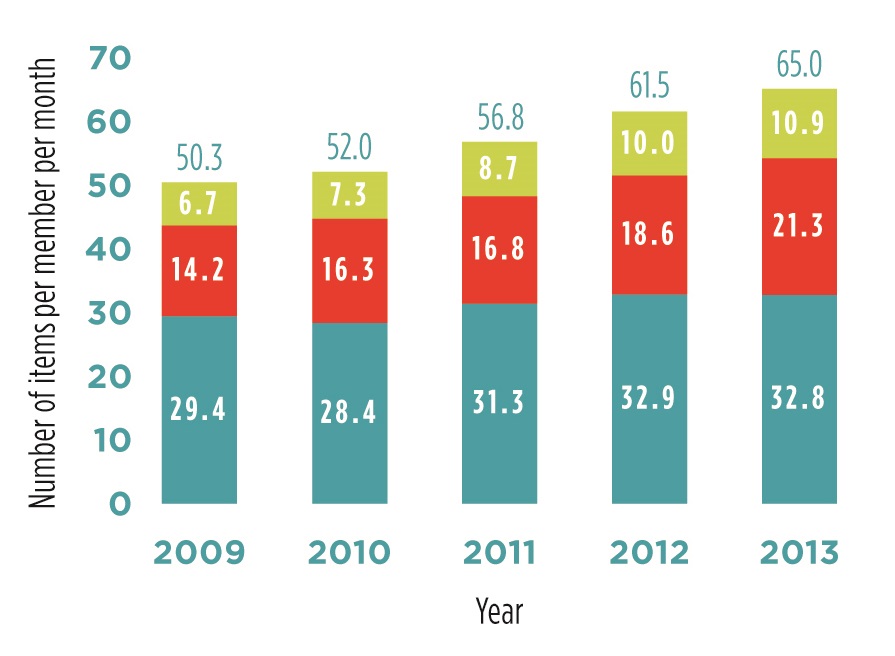

A somewhat surprising trend highlighted in the research is that the proliferation of delivery channels has actually led to an increase in total transactions. In fact, according to 2013 data from Fiserv, the average number of items per member increased 30% over the past four years as indicated in the accompanying chart.This trend can be summed up with another restaurant analogy that is used in the report. Think of a buffet. When additional food options are added, patrons generally don't consume less. In fact, when you offer more at the buffet, people consume more. So too is the case with banking delivery channels.

Certainly, while credit union members' plates have been piled higher with transactions during the past four years, the mix of transaction channels used has changed. Digital transactions grew 14.5% during the 12 months through May 2013, while ATM/debit usage grew only 9%. As the variety of delivery channels grows and the volume of total transactions increases, the cost of offering these options grows as well.

This isn't to say that credit unions face a fork in the road where they must select one of two distinct paths, leaving either branches or electronic channels behind to focus solely on the other. Rather, organizations must determine the appropriate value they will place on each delivery channel.

Access the full report here.

Andrew Downin is innovation director for the Filene Research Institute. He can be reached at 608-661-3746 or [email protected].

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.