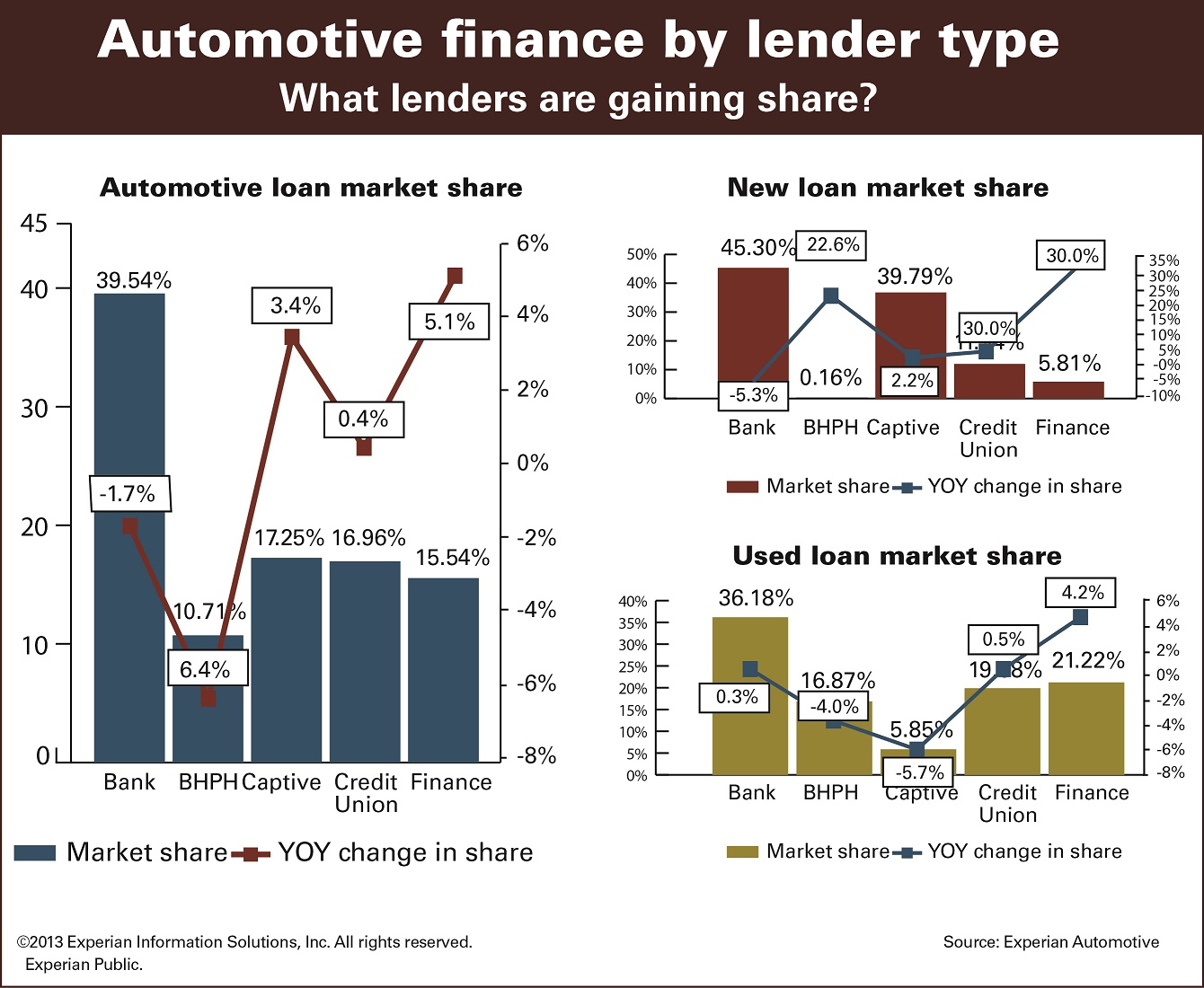

When it came to how lenders fared with auto lending market share in the first quarter, credit unions were ahead of finance companies and buy here/pay here financing lots.

According to Experian's State of the Automotive Finance Market report, credit unions had 16.7% market share compared to 15.5% for finance companies and 10.7% for buy here/pay here financing lots.

Banks led the pack at 39.5% followed by captive finance companies at 17.43%, the data showed.

Meanwhile, there's even more proof that credit unions are at the entry point of a trend that shows more consumers are buying and leasing new cars. Experian Automotive said new vehicle leasing rose by 12.5% in the first quarter to achieve the highest level since the company began tracking the data in 2006.

According to Experian's State of the Automotive Finance Market report, leasing accounted for a record 27.5% of all new vehicles financed, up from 24.4% in the first quarter of 2012.

(Click on the image to see expanded version.)

Additionally, findings from the report showed that the average monthly payment for a new vehicle financed in the first quarter was $459, down from $462 in the first quarter of 2012.

“Consumers tend to shop for vehicles based within the limits of their budget, and leasing is often seen as a viable path to a lower monthly payment,” said Melinda Zabritski, senior director of Experian Automotive Credit.

“Lenders have seen overall stability come back to the market since the recession, and leasing has gradually returned as a larger part of many lender strategies,” she added.

Experian said while leasing a vehicle can potentially help consumers achieve a lower monthly payment, the firm's data showed a rise in loan lengths to 65 months in the first quarter, up from 64 months in the first quarter of 2012, and a decrease in interest rates to 4.5%, was down from 4.6% for the same period last year.

The shifts have helped to keep payments low for new vehicles financed, according to Experian. In the first quarter, the average loan amount for a new vehicle financed increased by $628, going from $26,020 in the first quarter of 2012 to $26,648 in this year's first quarter. The average used vehicle loan increased $461, going from $17,071 to $17,532 for the same period.

An interesting wrinkle that has emerged within the bustle of new car financing is the rise of subprime loans. Experian found that consumers within all credit score tiers were able to obtain financing in the first quarter.

Most notably, loans going to consumers with credit outside of prime such as nonprime, subprime and deep subprime, jumped to 45.2% of the overall loan market in the first quarter, up from 44.4% for the same period in 2012.

The average credit score for a new vehicle loan dropped to 755 in the first quarter, which was down from 760 from the first quarter of 2012, according to Experian. There was a two-point drop from 659 to 657 seen in the average credit score for used vehicle loans for the same period.

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.