When you think of Gen Y’s preferred banking activity, the thought of waiting in the teller line at a branch doesn’t exactly come to mind.

But the latest Consumer Trends Survey from technology vendor Fiserv Inc. included a surprising result: Gen Y visits branches more than Gen X, Baby Boomers and seniors do.

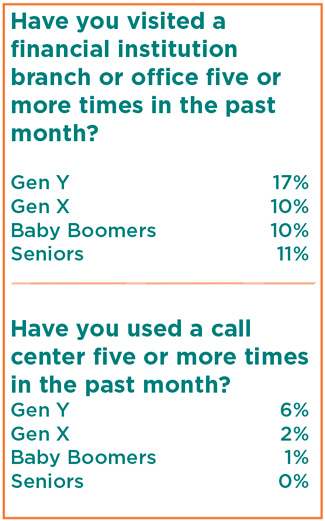

The data showed that 17% of Gen Y members visited a financial institution branch or office five or more times in the previous month, compared to Gen X’s 10%, Baby Boomers’ 10% and seniors’ 11%.

Daniel Steere, director of consumer insights at Fiserv, said it was the most surprising finding from the survey, which investigated consumer banking behavior by channel and age group.

“I was expecting to see Gen Y pushing trends toward the digital channel, and we did see that,” Steere said. “But they are still using channels that are high-cost to financial institutions, like call centers and branches.”

Steere said the survey’s Gen Y respondents were not asked why they are visiting branches and that Fiserv would like to examine that angle in the future. But he speculates that Gen Y’s branch visits are due to more complicated needs such as consultations for a first mortgage or auto loan, not routine transactions. Given that assumption, he believes credit unions should ensure their front line staff members are trained to educate young members.

“Based on my personal research, I don’t think anyone says that they love to go into a branch and stand in line,” Steere said. “I suspect that when Gen Y members go into a branch, it’s because they have a problem that they can’t solve.”

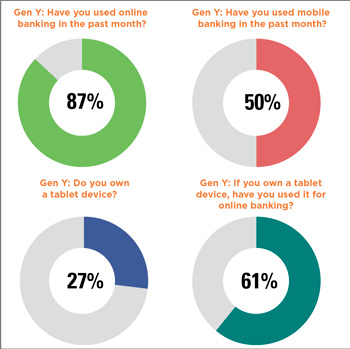

Fiserv also found that 87% of Gen Y members used online banking in the previous month and 50% of Gen Y members used mobile banking in the previous month, Steere said. Survey highlights also showed that 34% of Gen Y members are high volume ATM users, compared to Gen X’s 30%, Baby Boomers’ 22% and seniors’ 12%. Six percent of Gen Y members are high volume call center users, compared to Gen X’s 2%, Baby Boomers’ 1% and seniors’ 0%.

At MIT Federal Credit Union, a $335.6 million credit union in Cambridge, Mass., where students comprise approximately 28% of total membership, young members typically visit a branch once to set up their accounts and then turn to the comfort of their computers and smartphones for banking activities, said President/CEO Brian Ducharme.

“We’re set up for remote access,” Ducharme said. “Members can make deposits from our ATMs, and we’ll see students doing that when they’re only 10 yards away from a teller. They’re very comfortable with self-service.”

However, Ducharme said young members do value personal interaction. He said if a transaction is more complicated, they’ll use the credit union’s call center or visit a branch.

“It depends on the complexity of the transaction and sometimes on their comfort level,” he said. “For example, with a mortgage, they may want to talk to someone to better understand how to make payments and how it will affect their taxes.”

Ben Rogers, research director for the Filene Research Institute, agrees that Gen Y members only make trips to branches during exceptional circumstances, for example, to open a new account or solve a specific issue.

“It’s hard to characterize the whole group as valuing or not valuing in-person branches,” Rogers said. “It is safe to say, however, that they value them less than prior generations did, because they have not been conditioned to accept waiting in branches or conducting in-person or paper transactions that can be accomplished remotely.”

Rogers said Filene recently found that convenience is the No. 1 factor Gen Y considers when choosing a financial institution, followed by product features and service, and financial institutions must implement multiple channels to meet the need for convenience.

“It used to be your branch locations were the main driver of convenience, and then it became branches plus ATMs,” Rogers said. “But today, you have to consider technologies like mobile applications, remote check deposit and fast, functional web services.”

So which channels are priorities for Gen Y? Rogers said according to seven recent, in-depth interviews conducted with seven Gen Y members by bank and credit union-focused research company Facilitas, six of the seven listed ATM access as necessary and all seven said mobile banking apps are critical.

Steere emphasized the one device that credit unions should start putting on their radar are tablets. According to Consumer Trends Survey Results, 27% of Gen Y members own a tablet device and 61% of those Gen Y members said they had used the tablet for online banking. With their larger screens, tablets present an opportunity for CUs to share information in an interactive, engaging manner.

“Tablets are considered high priced, luxury items, so that data shocked me,” Steere said. “But Gen Y is all about the overall experience. In the future, I see mobile devices being used for quick transactions and tablets being used for more engaging experiences and rich interactions.”

Mobile alerts are another hot feature for Gen Y because they provide a sense of control, Steere added.

“Some Gen Y members are managing their finances on a tight margin of error and are checking their account balances 10 or 12 times a day,” Steere said. “Alerts can help them feel like they’re on top of things.”

Rogers added that according to a TowerGroup report, the number of interactions a consumer has with his or her financial institution per year is expected to double from 60 to 120 between 2007 and 2020. Mobile and online interactions are expected to increase while branch, ATM and call center interactions should remain roughly the same.

“In-person banking is not going away,” Rogers said. “It’s simply being placed as two–branch and contact center–parts of that five-part mix.”

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.

Natasha Chilingerian

Natasha Chilingerian has been immersed in the credit union industry for over a decade. She first joined CU Times in 2011 as a freelance writer, and following a two-year hiatus from 2013-2015, during which time she served as a communications specialist for Xceed Financial Credit Union (now Kinecta Federal Credit Union), she re-joined the CU Times team full-time as managing editor. She was promoted to executive editor in 2019. In the earlier days of her career, Chilingerian focused on news and lifestyle journalism, serving as a writer and editor for numerous regional publications in Oregon, Louisiana, South Carolina and the San Francisco Bay Area. In addition, she holds experience in marketing copywriting for companies in the finance and technology space. At CU Times, she covers People and Community news, cybersecurity, fintech partnerships, marketing, workplace culture, leadership, DEI, branch strategies, digital banking and more. She currently works remotely and splits her time between Southern California and Portland, Ore.