Late last year the NCUA published its regulation on expectations for credit union directors. The agency focused specifically on financial literacy and how it will be measured. As the July 27 deadline for compliance looms, Credit Union Leadership Forum conducted a survey of credit union executives and board members as well as numerous interviews about the NCUA regulations and the state of director literacy.

Following the financial crisis, the role of all directors has forever been changed in fundamental ways. Among credit unions, there is a frustration that traces back to annoyance with the NCUA's dictates.

Nobody disputes that financial literacy is a must have for credit union directors, but beyond agreement on that, it's a fast plunge into acrimony and discord.

So, what did the survey uncover? With around 100 respondents, split between board members and chief executives of credit unions, who answered 29 questions, there was plenty of room for debate.

When asked to rate the effectiveness of their boards, 58% called their boards “very effective,” 36% said the board was “somewhat effective.” The remaining 6% said their boards were “not effective.”

Another question asked respondents to list board committees. A supervisory committee was the popular with 89%. An asset-liability committee was No. 2 with 59%.

Todd Sprang, an accountant in Clifton Gunderson's Oak Brook, Ill., office was struck that only 6% of the respondents said they had a risk committee. “A trend we will see in more credit unions is that they will have risk committees with oversight of the risks the institution takes,” predicted Sprang.

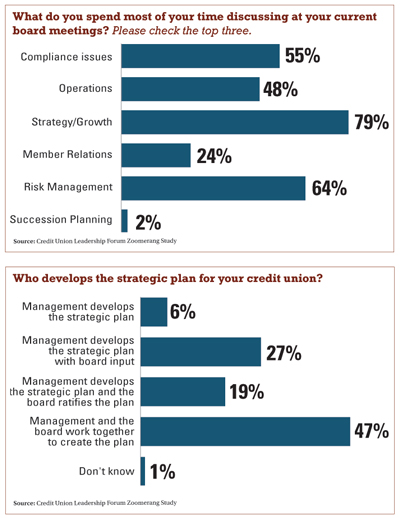

“Who develops the strategic plan for your credit union?” elicited more contention. The responses revealed a lack of agreement in the industry about the locus of responsibility for strategy. “Management and the board work together to create the plan” captured 47% or responses. “Management develops the strategic plan with board input” was No. 2 with 27%.

Observers also raised eyebrows to responses to: “Does your credit union perform an annual evaluation of board committees?” That's because 77% said no.

The next question, “Does your credit union perform evaluations of individual board members?” found a large majority, 88%, said no.

But evaluation is increasingly emerging as a hot topic in credit union board composition. Brian Barnier, an executive with ValueBridge Advisors, wrote this in an email: “Less than a quarter of boards are conducting annual board performance reviews. Boards are missing golden opportunities to use board performance reviews to identify gaps in areas such as strategy and risk insight, then close those with recruitment and education. With skills in place, CUs can more easily conduct strategy workshops to drive toward more liquid and profitable growth to meet the needs of current and future members.”

Steve Winninger, CEO of the $1.5 billion Lake Trust Credit Union in Lansing, Mich., in an interview elaborated on Barnier's point, saying, “For an effective board you need the right people. Boards have to become proactive in recruiting new board members who bring needed skills.” Boards increasingly need a range of skills and smart boards, per Winninger. They have to identify a need–say, marketing expertise or familiarity with mobile technologies–then go out hunting for people with the needed skills. And that is a big change from the old ways of filling board vacancies.

needed skills. And that is a big change from the old ways of filling board vacancies.

Responses to question 22 triggered another round of concern: “What do you spend most of your time discussing at your current board meetings? Pick the top three.” Strategy/growth topped this list at 79%, while risk management and compliance rounded out the top three at 64% and 55%, respectively. Operations ranked next at 48% followed by member relations at 24%. Succession planning captured just 2%.

Commented Marty Goldman, a longtime board member at Marine Federal Credit Union, a $569 million institution headquartered in Jacksonville, N.C., “I am surprised strategy/growth was No. 1 and compliance is down the list.”

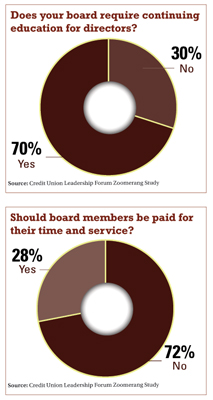

Responses to, “Does your board require continuing education for directors?” provoked more surprise. Seventy percent answered that it was required, but a full 30% said it was not required. One expert questioned how one in three credit unions could not require continuing education.

“That really disappointed me,” Goldman added.

The tradition of volunteer directors runs deep in the credit union world, as responses demonstrated. Just 28% said credit union board members should be paid and the remaining 72% answered they should not.

It is not just the role of directors in isolation that now is under review. Also in play is the delicate relationship between board members and credit union management. Some insist the varying roles are clear. “There's a big gulf between management and governance, which is the board's job. Management is about implementing the board's vision,” said Lake Trust's Winninger.

Blunter is the analysis offered by Dave Osborn, CEO of Anheuser-Busch Employees' Credit Union, a $1.3 billion credit union in St. Louis. He explained, “Boards focus on what, management focuses on how.” That might be clear in theory but, Osborn admitted, it's not hard for boards to stray across the line and get mired in operations. That's why Osborn recommends that top credit union executives themselves serve on boards. “I've been on the Co-Op Financial Services board and also on Missouri Corporate's. Sometimes as a board member you just have to bite your tongue and you learn that in board service,” he said.

The survey did not directly ask how people felt about NCUA's demand for heightened director literacy, but some respondents suggested perhaps it should have. Opinions on this are hotly divided.

Some directors applaud what the NCUA is doing. Chuck Scheithauer, treasurer of the board of directors at the $630 million CoastHills Federal Credit Union in central California, said, “I took the NCUA test for director financial literacy. I thought it would be a pushover; it wasn't.” He added that all the members of his board have taken literacy classes, said Scheithauer, and the upshot is that this is a board that genuinely understands the key ratios, what they mean, and why they matter. “I think it is good for NCUA to push for more literacy.”

But Don Oliver, board president at the tiny Greater Abyssinia Credit Union in Cleveland, with 380 members and assets under $1 million, lamented “I feel NCUA is trying to decrease the number of small credit unions.” A particular sticking point with him was the tight deadline for director financial literacy. “A year would have been fairer,” said Oliver. He claimed his credit union's directors would make the deadline but it won't be easy. He also believes many directors on other boards of small credit unions will have to step down before the year is up. “Are we losing touch with the human side of credit unions?” he asked.

Oliver is not alone. Mansel Guerry, CEO of $29 million Brightview Credit Union in Mississippi and chairman of the Credit Union 24 board of directors, said, “There is a disconnect between regulation and reality. The water level is rising and it is drowning what this industry started out to do. NCUA will scratch its head and wonder where all the credit unions below $25 million went. The answer is: you buried them.”

NCUA was not alone in winning criticism. Marine Federal's Marty Goldman caustically grumbled, “The [industry] trade organizations leaped on the NCUA ruling as a money maker, rushing to offer classes to directors. I find that unfortunate.”

But do note, not everybody blames NCUA or points blaming fingers at the industry associations. Mike Hanson, CEO of Massachusetts Credit Union Insurance Corp., a quasi-private insurance provider in Westborough, Mass., said that the trend toward better informed, more involved and active credit union boards has been a long time in the making. “The NCUA regs sparked interest but this has been happening for some years. The business is more complicated, and boards have had to respond. Boards have been getting better over the long haul and more credit unions have been spending more time building good boards.”

Winninger too saw a trend for board improvement. “If one issue stands out for me, it is the notion of boards doing self-monitoring. I think it is a very good thing, and it needs to be effective. If an employee is not performing, their manager generally knows it early and has the authority to address it. If a board member is not performing at an effective level, their manager (the members) generally won't know it unless the credit union is publicly in trouble. That leaves the action up to the peers, who are also generally friends and volunteers, so it takes courage to take on those issues. It is very easy to tolerate less than effective governance in this situation, so rigorous self-monitoring is not only hard, but extremely critical.”

Looking to the future, MSIC's Hanson said, “A lot of institutions have been working on this and we are moving in the right direction. There are problems. We have a long way to go, but we are moving.”

The other indisputable take away? “Governance will become a bigger and bigger deal,” said Barnier. “And it is proving difficult to get people skilled up.”

Complete your profile to continue reading and get FREE access to CUTimes.com, part of your ALM digital membership.

Your access to unlimited CUTimes.com content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Breaking credit union news and analysis, on-site and via our newsletters and custom alerts

- Weekly Shared Accounts podcast featuring exclusive interviews with industry leaders

- Educational webcasts, white papers, and ebooks from industry thought leaders

- Critical coverage of the commercial real estate and financial advisory markets on our other ALM sites, GlobeSt.com and ThinkAdvisor.com

Already have an account? Sign In Now

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.